8.2: 8.2 Deriving OLS Estimators

- Page ID

- 7240

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Now that we have developed some of the rules for differential calculus, we can see how OLS finds values of ^αα^ and ^ββ^ that minimize the sum of the squared error. In formal terms, let’s define the set, S(^α,^β)S(α^,β^), as a pair of regression estimators that jointly determine the residual sum of squares given that: Yi=^Yi+ϵi=^α+^βXi+ϵiYi=Y^i+ϵi=α^+β^Xi+ϵi. This function can be expressed:

S(^α,^β)=n∑i=1ϵ2i=∑(Yi−^Yi)2=∑(Yi−^α−^βXi)2S(α^,β^)=∑i=1nϵi2=∑(Yi−Yi^)2=∑(Yi−α^−β^Xi)2

First, we will derive ^αα^.

8.2.1 OLS Derivation of ^αα^

Take the partial derivatives of S(^α,^β)S(α^,β^) with-respect-to (w.r.t) ^αα^ in order to determine the formulation of ^αα^ that minimizes S(^α,^β)S(α^,β^). Using the chain rule,

∂S(^α,^β)∂^α=∑2(Yi−^α−^βXi)2−1∗(Yi−^α−^βXi)′=∑2(Yi−^α−^βXi)1∗(−1)=−2∑(Yi−^α−^βXi)=−2∑Yi+2n^α+2^β∑Xi∂S(α^,β^)∂α^=∑2(Yi−α^−β^Xi)2−1∗(Yi−α^−β^Xi)′=∑2(Yi−α^−β^Xi)1∗(−1)=−2∑(Yi−α^−β^Xi)=−2∑Yi+2nα^+2β^∑Xi

Next, set the derivative equal to 00.

∂S(^α,^β)∂^α=−2∑Yi+2n^α+2^β∑Xi=0∂S(α^,β^)∂α^=−2∑Yi+2nα^+2β^∑Xi=0

Then, shift non-^αα^ terms to the other side of the equal sign:

2n^α=2∑Yi−2^β∑Xi2nα^=2∑Yi−2β^∑XiFinally, divide through by 2n2n:2n^α2n=2∑Yi−2^β∑Xi2nA=∑Yin−^β∗∑Xin=¯Y−^β¯X2nα^2n=2∑Yi−2β^∑Xi2nA=∑Yin−β^∗∑Xin=Y¯−β^X¯∴^α=¯Y−^β¯X(8.1)(8.1)∴α^=Y¯−β^X¯

8.2.2 OLS Derivation of ^ββ^

Having found ^αα^, the next step is to derive ^ββ^. This time we will take the partial derivative w.r.t ^ββ^. As you will see, the steps are a little more involved for ^ββ^ than they were for ^αα^.

∂S(^α,^β)∂^β=∑2(Yi−^α−^βXi)2−1∗(Yi−^α−^βXi)′=∑2(Yi−^α−^βXi)1∗(−Xi)=2∑(−XiYi+^αXi+^βX2i)=−2∑XiYi+2^α∑Xi+2^β∑X2i∂S(α^,β^)∂β^=∑2(Yi−α^−β^Xi)2−1∗(Yi−α^−β^Xi)′=∑2(Yi−α^−β^Xi)1∗(−Xi)=2∑(−XiYi+α^Xi+β^Xi2)=−2∑XiYi+2α^∑Xi+2β^∑Xi2

Since we know that ^α=¯Y−^β¯Xα^=Y¯−β^X¯, we can substitute ¯Y−^β¯XY¯−β^X¯ for ^αα^.

∂S(^α,^β)∂^β=−2∑XiYi+2(¯Y−^β¯X)∑Xi+2^β∑X2i=−2∑XiYi+2¯Y∑Xi−2^β¯X∑Xi+2^β∑X2i∂S(α^,β^)∂β^=−2∑XiYi+2(Y¯−β^X¯)∑Xi+2β^∑Xi2=−2∑XiYi+2Y¯∑Xi−2β^X¯∑Xi+2β^∑Xi2

Next, we can substitute ∑Yin∑Yin for ¯YY¯ and ∑Xin∑Xin for ¯XX¯ and set it equal to 00.

∂S(^α,^β)∂^β=−2∑XiYi+2∑Yi∑Xin−2^β∑Xi∑Xin+2^β∑X2i=0∂S(α^,β^)∂β^=−2∑XiYi+2∑Yi∑Xin−2β^∑Xi∑Xin+2β^∑Xi2=0

Then, multiply through by n2n2 and put all the ^ββ^ terms on the same side.

n^β∑X2i−^β(∑Xi)2=n∑XiYi−∑Xi∑Yi^β(n∑X2i−(∑Xi)2)=n∑XiYi−∑Xi∑Yi∴^β=n∑XiYi−∑Xi∑Yin∑X2i−(∑Xi)2nβ^∑Xi2−β^(∑Xi)2=n∑XiYi−∑Xi∑Yiβ^(n∑Xi2−(∑Xi)2)=n∑XiYi−∑Xi∑Yi∴β^=n∑XiYi−∑Xi∑Yin∑Xi2−(∑Xi)2

The ^ββ^ term can be rearranged such that:

^β=Σ(Xi−¯X)(Yi−¯Y)Σ(Xi−¯X)2(8.2)(8.2)β^=Σ(Xi−X¯)(Yi−Y¯)Σ(Xi−X¯)2

Now remember what we are doing here: we used the partial derivatives for ∑ϵ2∑ϵ2 with respect to ^αα^ and ^ββ^ to find the values for ^αα^ and ^ββ^ that will give us the smallest value for ∑ϵ2∑ϵ2. Put differently, the formulas for ^ββ^ and ^αα^ allow the calculation of the error-minimizing slope (change in YY given a one-unit change in XX) and intercept (value for YY when XX is zero) for any data set representing a bivariate, linear relationship. No other formulas will give us a line, using the same data, that will result in as small a squared-error. Therefore, OLS is referred to as the Best Linear Unbiased Estimator (BLUE).

8.2.3 Interpreting ^ββ^ and ^αα^

In a regression equation, Y=^α+^βXY=α^+β^X, where ^αα^ is shown in Equation (8.1) and ^ββ^ is shown in Equation (8.2). Equation (8.2) shows that for each 1-unit increase in XX you get ^ββ^ units to change in YY. Equation (8.1) shows that when XX is 00, YY is equal to ^αα^. Note that in a regression model with no independent variables, ^αα^ is simply the expected value (i.e., mean) of YY.

The intuition behind these formulas can be shown by using R to calculate “by hand” the slope (^ββ^) and intercept (^αα^) coefficients. A theoretical simple regression model is structured as follows:

Yi=α+βXi+ϵiYi=α+βXi+ϵi

- αα and ββ are constant terms

- αα is the intercept

- ββ is the slope

- XiXi is a predictor of YiYi

- ϵϵ is the error term

The model to be estimated is expressed as Y=^β+^βX+/epsilonY=β^+β^X+/epsilon.

As noted, the goal is to calculate the intercept coefficient:

^α=¯Y−^β¯Xα^=Y¯−β^X¯and the slope coefficient:^β=Σ(Xi−¯X)(Yi−¯Y)Σ(Xi−¯X)2β^=Σ(Xi−X¯)(Yi−Y¯)Σ(Xi−X¯)2

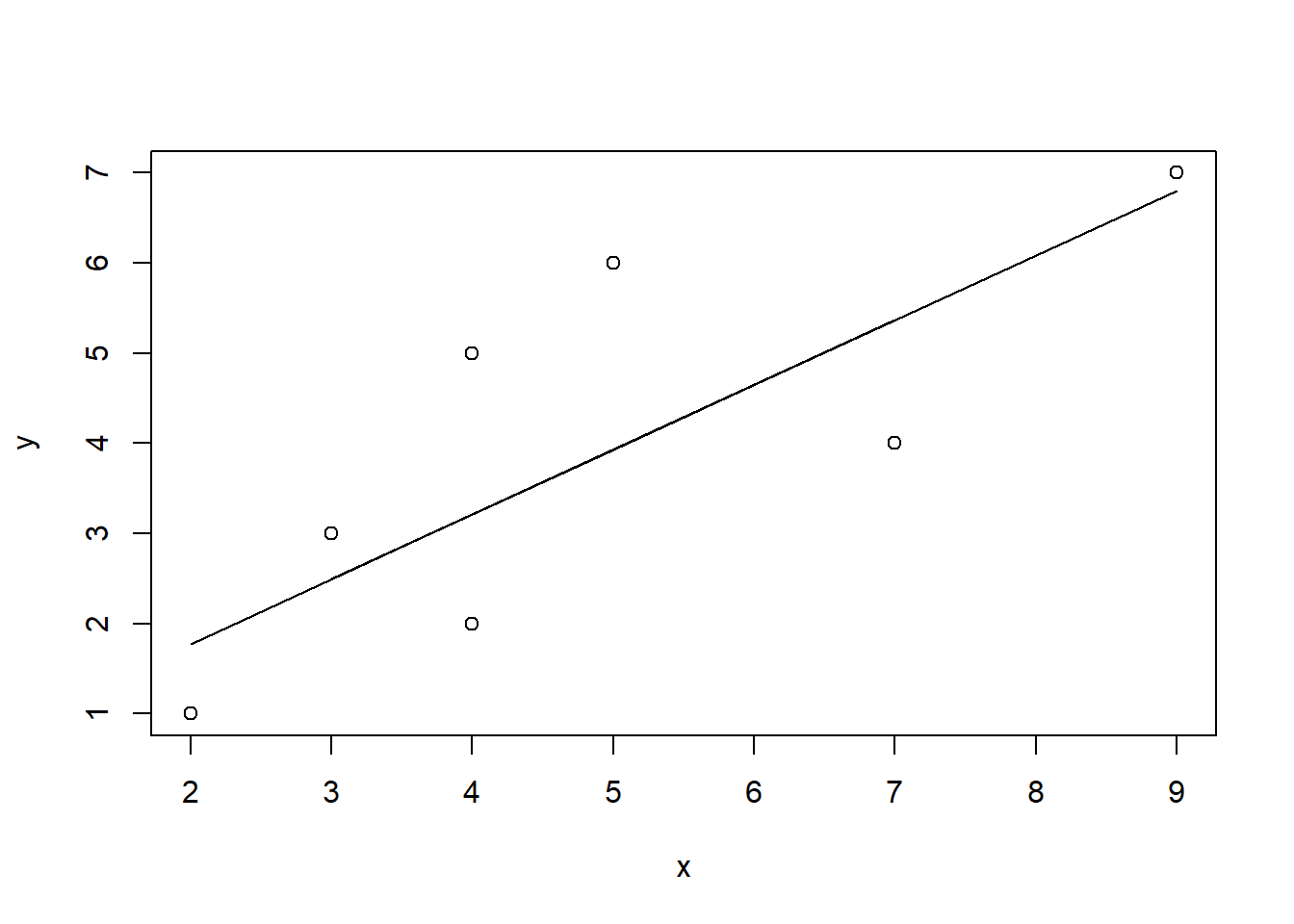

Using R, this can be accomplished in a few steps. First, create a vector of values for x and y (note that we chose these values arbitrarily for the purpose of this example).

x <- c(4,2,4,3,5,7,4,9)

x## [1] 4 2 4 3 5 7 4 9y <- c(2,1,5,3,6,4,2,7)

y## [1] 2 1 5 3 6 4 2 7Then, create objects for ¯XX¯ and ¯YY¯:

xbar <- mean(x)

xbar## [1] 4.75ybar <- mean(y)

ybar## [1] 3.75Next, create objects for (X−¯X)(X−X¯) and (Y−¯Y)(Y−Y¯), the deviations of XX and YY around their means:

x.m.xbar <- x-xbar

x.m.xbar## [1] -0.75 -2.75 -0.75 -1.75 0.25 2.25 -0.75 4.25y.m.ybar <- y-ybar

y.m.ybar## [1] -1.75 -2.75 1.25 -0.75 2.25 0.25 -1.75 3.25Then, calculate ^ββ^:

^β=Σ(Xi−¯X)(Yi−¯Y)Σ(Xi−¯X)2β^=Σ(Xi−X¯)(Yi−Y¯)Σ(Xi−X¯)2

B <- sum((x.m.xbar)*(y.m.ybar))/sum((x.m.xbar)^2)

B## [1] 0.7183099Finally, calculate ^αα^

^α=¯Y−^β¯Xα^=Y¯−β^X¯

A <- ybar-B*xbar

A## [1] 0.3380282To see the relationship, we can produce a scatterplot of x and y and add our regression line, as shown in Figure \(\PageIndex{4}\). So, for each unit increase in xx, yy increases by 0.7183099 and when xx is 00, yy is equal to 0.3380282.

plot(x,y)

lines(x,A+B*x)

dev.off()## RStudioGD

## 2