14.1: Introduction to Multiple Regression

- Page ID

- 36185

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\( \newcommand{\id}{\mathrm{id}}\) \( \newcommand{\Span}{\mathrm{span}}\)

( \newcommand{\kernel}{\mathrm{null}\,}\) \( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\) \( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\) \( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\id}{\mathrm{id}}\)

\( \newcommand{\Span}{\mathrm{span}}\)

\( \newcommand{\kernel}{\mathrm{null}\,}\)

\( \newcommand{\range}{\mathrm{range}\,}\)

\( \newcommand{\RealPart}{\mathrm{Re}}\)

\( \newcommand{\ImaginaryPart}{\mathrm{Im}}\)

\( \newcommand{\Argument}{\mathrm{Arg}}\)

\( \newcommand{\norm}[1]{\| #1 \|}\)

\( \newcommand{\inner}[2]{\langle #1, #2 \rangle}\)

\( \newcommand{\Span}{\mathrm{span}}\) \( \newcommand{\AA}{\unicode[.8,0]{x212B}}\)

\( \newcommand{\vectorA}[1]{\vec{#1}} % arrow\)

\( \newcommand{\vectorAt}[1]{\vec{\text{#1}}} % arrow\)

\( \newcommand{\vectorB}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vectorC}[1]{\textbf{#1}} \)

\( \newcommand{\vectorD}[1]{\overrightarrow{#1}} \)

\( \newcommand{\vectorDt}[1]{\overrightarrow{\text{#1}}} \)

\( \newcommand{\vectE}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash{\mathbf {#1}}}} \)

\( \newcommand{\vecs}[1]{\overset { \scriptstyle \rightharpoonup} {\mathbf{#1}} } \)

\( \newcommand{\vecd}[1]{\overset{-\!-\!\rightharpoonup}{\vphantom{a}\smash {#1}}} \)

\(\newcommand{\avec}{\mathbf a}\) \(\newcommand{\bvec}{\mathbf b}\) \(\newcommand{\cvec}{\mathbf c}\) \(\newcommand{\dvec}{\mathbf d}\) \(\newcommand{\dtil}{\widetilde{\mathbf d}}\) \(\newcommand{\evec}{\mathbf e}\) \(\newcommand{\fvec}{\mathbf f}\) \(\newcommand{\nvec}{\mathbf n}\) \(\newcommand{\pvec}{\mathbf p}\) \(\newcommand{\qvec}{\mathbf q}\) \(\newcommand{\svec}{\mathbf s}\) \(\newcommand{\tvec}{\mathbf t}\) \(\newcommand{\uvec}{\mathbf u}\) \(\newcommand{\vvec}{\mathbf v}\) \(\newcommand{\wvec}{\mathbf w}\) \(\newcommand{\xvec}{\mathbf x}\) \(\newcommand{\yvec}{\mathbf y}\) \(\newcommand{\zvec}{\mathbf z}\) \(\newcommand{\rvec}{\mathbf r}\) \(\newcommand{\mvec}{\mathbf m}\) \(\newcommand{\zerovec}{\mathbf 0}\) \(\newcommand{\onevec}{\mathbf 1}\) \(\newcommand{\real}{\mathbb R}\) \(\newcommand{\twovec}[2]{\left[\begin{array}{r}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\ctwovec}[2]{\left[\begin{array}{c}#1 \\ #2 \end{array}\right]}\) \(\newcommand{\threevec}[3]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\cthreevec}[3]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \end{array}\right]}\) \(\newcommand{\fourvec}[4]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\cfourvec}[4]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \end{array}\right]}\) \(\newcommand{\fivevec}[5]{\left[\begin{array}{r}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\cfivevec}[5]{\left[\begin{array}{c}#1 \\ #2 \\ #3 \\ #4 \\ #5 \\ \end{array}\right]}\) \(\newcommand{\mattwo}[4]{\left[\begin{array}{rr}#1 \amp #2 \\ #3 \amp #4 \\ \end{array}\right]}\) \(\newcommand{\laspan}[1]{\text{Span}\{#1\}}\) \(\newcommand{\bcal}{\cal B}\) \(\newcommand{\ccal}{\cal C}\) \(\newcommand{\scal}{\cal S}\) \(\newcommand{\wcal}{\cal W}\) \(\newcommand{\ecal}{\cal E}\) \(\newcommand{\coords}[2]{\left\{#1\right\}_{#2}}\) \(\newcommand{\gray}[1]{\color{gray}{#1}}\) \(\newcommand{\lgray}[1]{\color{lightgray}{#1}}\) \(\newcommand{\rank}{\operatorname{rank}}\) \(\newcommand{\row}{\text{Row}}\) \(\newcommand{\col}{\text{Col}}\) \(\renewcommand{\row}{\text{Row}}\) \(\newcommand{\nul}{\text{Nul}}\) \(\newcommand{\var}{\text{Var}}\) \(\newcommand{\corr}{\text{corr}}\) \(\newcommand{\len}[1]{\left|#1\right|}\) \(\newcommand{\bbar}{\overline{\bvec}}\) \(\newcommand{\bhat}{\widehat{\bvec}}\) \(\newcommand{\bperp}{\bvec^\perp}\) \(\newcommand{\xhat}{\widehat{\xvec}}\) \(\newcommand{\vhat}{\widehat{\vvec}}\) \(\newcommand{\uhat}{\widehat{\uvec}}\) \(\newcommand{\what}{\widehat{\wvec}}\) \(\newcommand{\Sighat}{\widehat{\Sigma}}\) \(\newcommand{\lt}{<}\) \(\newcommand{\gt}{>}\) \(\newcommand{\amp}{&}\) \(\definecolor{fillinmathshade}{gray}{0.9}\)Multiple regression extends simple two-variable regression to the case that still has one response but many predictors (denoted \(x_1, x_2, x_3, \dots\)). The method is motivated by scenarios where many variables may be simultaneously connected to an output.

We will consider Ebay auctions of a video game called Mario Kart for the Nintendo Wii. The outcome variable of interest is the total price of an auction, which is the highest bid plus the shipping cost. We will try to determine how total price is related to each characteristic in an auction while simultaneously controlling for other variables. For instance, all other characteristics held constant, are longer auctions associated with higher or lower prices? And, on average, how much more do buyers tend to pay for additional Wii wheels(plastic steering wheels that attach to the Wii controller) in auctions? Multiple regression will help us answer these and other questions.

The data set mario kart includes results from 141 auctions.1 Four observations from this data set are shown in Table \(\PageIndex{1}\), and descriptions for each variable are shown in Table \(\PageIndex{2}\). Notice that the condition and stock photo variables are indicator variables. For instance, the cond new variable takes value 1 if the game up for auction is new and 0 if it is used. Using indicator variables in place of category names allows for these variables to be directly used in regression. See Section 7.2.7 for additional details. Multiple regression also allows for categorical variables with many levels, though we do not have any such variables in this analysis, and we save these details for a second or third course.

1Diez DM, Barr CD, and Cetinkaya-Rundel M. 2012. openintro: OpenIntro data sets and supplemental functions. cran.r-project.org/web/packages/openintro.

| price | cond new | stock photo | duration | wheels | |

|---|---|---|---|---|---|

| 1 | 51.55 | 1 | 1 | 3 | 1 |

| 2 | 37.04 | 0 | 1 | 3 | 1 |

| \(\vdots\) | \(\vdots\) | \(\vdots\) | \(\vdots\) | \(\vdots\) | \(\vdots\) |

| 140 | 38.76 | 0 | 0 | 7 | 0 |

| 141 | 54.51 | 1 | 1 | 1 | 2 |

| variable | description |

|---|---|

| price | final auction price plus shipping costs, in US dollars |

| cond_new | a coded two-level categorical variable, which takes value 1 when the game is new and 0 if the game is used |

| stock_photo | a coded two-level categorical variable, which takes value 1 if the primary photo used in the auction was a stock photo and 0 if the photo was unique to that auction |

| duration | the length of the auction, in days, taking values from 1 to 10 |

| wheels | the number of Wii wheels included with the auction (a Wii wheel is a plastic racing wheel that holds the Wii controller and is an optional but helpful accessory for playing Mario Kart) |

A Single-Variable Model for the Mario Kart Data

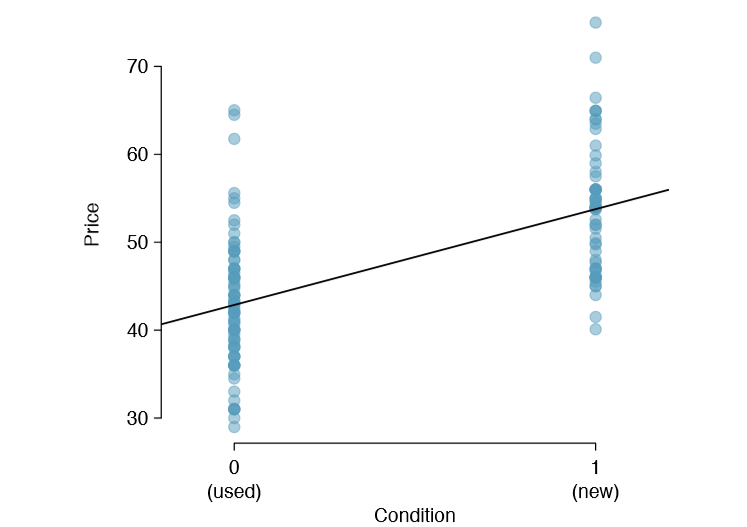

Let's fit a linear regression model with the game's condition as a predictor of auction price. The model may be written as

\[\hat {price} = 42.87 + 10.90 \times \text {cond_ new}\]

Results of this model are shown in Table \(\PageIndex{3}\) and a scatterplot for price versus game condition is shown in Figure \(\PageIndex{4}\).

| Estimate | Std. Error | t value | Pr(>|t|) | |

|---|---|---|---|---|

| (Intercept) | 42.8711 | 0.8140 | 52.67 | 0.0000 |

| cond_new | 10.8996 | 1.2583 | 8.66 | 0.0000 |

Exercise \(\PageIndex{1}\)

Figure \(\PageIndex{4}\). Does the linear model seem reasonable?

Answer

Yes. Constant variability, nearly normal residuals, and linearity all appear reasonable.

Exercise \(\PageIndex{2}\)

Interpret the coefficient for the game's condition in the model. Is this coefficient significantly different from 0?

Note that cond new is a two-level categorical variable that takes value 1 when the game is new and value 0 when the game is used. So 10.90 means that the model predicts an extra $10.90 for those games that are new versus those that are used. (See Section 7.2.7 for a review of the interpretation for two-level categorical predictor variables.) Examining the regression output in Table \(\PageIndex{3}\), we can see that the p-value for cond new is very close to zero, indicating there is strong evidence that the coefficient is different from zero when using this simple one-variable model.

Including and Assessing Many Variables in a Model

Sometimes there are underlying structures or relationships between predictor variables. For instance, new games sold on Ebay tend to come with more Wii wheels, which may have led to higher prices for those auctions. We would like to fit a model that includes all potentially important variables simultaneously. This would help us evaluate the relationship between a predictor variable and the outcome while controlling for the potential influence of other variables. This is the strategy used in multiple regression. While we remain cautious about making any causal interpretations using multiple regression, such models are a common first step in providing evidence of a causal connection.

We want to construct a model that accounts for not only the game condition, as in Section 8.1.1, but simultaneously accounts for three other variables: stock photo, duration, and wheels.

\[\hat {price} = \beta _0 + \beta _1 \times \text {cond_ new} + \beta _2 \times \text {stock_ photo} + \beta _3 \times \text {duration} + \beta _4 \times \text {wheels}\]

\[\hat {y} = \beta _0 + \beta _1x_1 + \beta _2x_2 + \beta _3x_3 + \beta _4x_4 \label {8.3}\]

In this equation, \(y\) represents the total price, \(x_1\) indicates whether the game is new, \(x_2\) indicates whether a stock photo was used, \(x_3\) is the duration of the auction, and \(x_4\) is the number of Wii wheels included with the game. Just as with the single predictor case, a multiple regression model may be missing important components or it might not precisely represent the relationship between the outcome and the available explanatory variables.

While no model is perfect, we wish to explore the possibility that this one may fit the data reasonably well.

We estimate the parameters \(\beta _0, \beta _1, \dots, \beta _4\) in the same way as we did in the case of a single predictor. We select \(b_0, b_1,\dots, b_4\) that minimize the sum of the squared residuals:

\[SSE = e^2_1 + e^2_2 + \dots + e^2_{141} = \sum \limits ^{141}_{i=1} e^2_i = \sum \limits ^{141}_{i=1} {(y_i - \hat {y}_i)}^2 \label {8.4}\]

Here there are 141 residuals, one for each observation. We typically use a computer to minimize the sum in Equation (8.4) and compute point estimates, as shown in the sample output in Table \(\PageIndex{5}\). Using this output, we identify the point estimates \(b_i\) of each \(\beta _i\), just as we did in the one-predictor case.

| Estimate | Std. Error | t value |

Pr(>|t|) |

|

|---|---|---|---|---|

|

(Intercept) cond_new stock_photo duration wheels |

36.2110 5.1306 1.0803 -0.0268 7.2852 |

1.5140 1.0511 1.0568 0.1904 0.5547 |

23.92 4.88 1.02 -0.14 13.13 |

0.0000 0.0000 0.3085 0.8882 0.0000 |

Multiple regression model

A multiple regression model is a linear model with many predictors. In general, we write the model as

\[\hat {y} = \beta _0 + \beta _1x_1 + \beta _2x_2 + \dots + \beta _kx_k\]

when there are k predictors. We often estimate the \(\beta _i\) parameters using a computer.

Exercise \(\PageIndex{3}\)

Write out the model in Equation (8.3) using the point estimates from Table \(\PageIndex{5}\). How many predictors are there in this model?3

Answer

\(\hat {y} = 36.21 + 5.13x_1 + 1.08x_2 - 0.03x_3 + 7.29x_4\), and there are k = 4 predictor variables.

Exercise \(\PageIndex{4}\)

What does \(\beta _4\), the coefficient of variable \(x_4\) (Wii wheels), represent? What is the point estimate of \(\beta _4\)?

Answer

It is the average difference in auction price for each additional Wii wheel included when holding the other variables constant. The point estimate is \(b_4 = 7.29\).

Exercise \(\PageIndex{5}\)

Compute the residual of the first observation in Table \(\PageIndex{1}\) on page 355 using the equation identified in Exercise 8.5.

Answer

\(e_i = y_i - \hat {y}_i = 51.55 - 49.62 = 1.93\), where 49.62 was computed using the variables values from the observation and the equation identified in Exercise \(\PageIndex{3}\).

Example \(\PageIndex{1}\)

We estimated a coefficient for cond new in Section 8.1.1 of \(b_1 = 10.90\) with a standard error of \(SE_{b1} = 1.26\) when using simple linear regression. Why might there be a difference between that estimate and the one in the multiple regression setting?

If we examined the data carefully, we would see that some predictors are correlated. For instance, when we estimated the connection of the outcome price and predictor cond new using simple linear regression, we were unable to control for other variables like the number of Wii wheels included in the auction. That model was biased by the confounding variable wheels. When we use both variables, this particular underlying and unintentional bias is reduced or eliminated (though bias from other confounding variables may still remain).

Example \(\PageIndex{1}\) describes a common issue in multiple regression: correlation among predictor variables. We say the two predictor variables are collinear (pronounced as co-linear) when they are correlated, and this collinearity complicates model estimation. While it is impossible to prevent collinearity from arising in observational data, experiments are usually designed to prevent predictors from being collinear.

Exercise \(\PageIndex{6}\)

The estimated value of the intercept is 36.21, and one might be tempted to make some interpretation of this coefficient, such as, it is the model's predicted price when each of the variables take value zero: the game is used, the primary image is not a stock photo, the auction duration is zero days, and there are no wheels included. Is there any value gained by making this interpretation?

Solution

Three of the variables (cond new, stock photo, and wheels) do take value 0, but the auction duration is always one or more days. If the auction is not up for any days, then no one can bid on it! That means the total auction price would always be zero for such an auction; the interpretation of the intercept in this setting is not insightful.

Adjusted R2 as a better estimate of explained variance

We first used R2 in Section 7.2 to determine the amount of variability in the response that was explained by the model:

\[R^2 = 1 - \dfrac {\text {variability in residuals}}{\text {variability in the outcome}} = 1 - \dfrac {V ar(e_i)}{V ar(y_i)}\]

where \(e_i\) represents the residuals of the model and yi the outcomes. This equation remains valid in the multiple regression framework, but a small enhancement can often be even more informative.

Exercise \(\PageIndex{7}\)

The variance of the residuals for the model given in Exercise 8.7 is 23.34, and the variance of the total price in all the auctions is 83.06. Calculate \(R^2\) for this model.

Solution

\(R^2 = 1 - \dfrac {23.34}{83.06} = 0.719\).

This strategy for estimating \(R^2\) is acceptable when there is just a single variable. However, it becomes less helpful when there are many variables. The regular \(R^2\) is actually a biased estimate of the amount of variability explained by the model. To get a better estimate, we use the adjusted \(R^2\).

Adjusted \(R^2\) as a tool for model assessment

The adjusted \(R^2\) is computed as

\[R^2_{adj} = 1 - \dfrac {\dfrac {V ar(e_i)}{(n - k - 1)}}{\dfrac {V ar(y_i)}{(n - 1)}} = 1 - \dfrac {V ar(e_i)}{V ar(y_i)} \times \dfrac {n - 1}{n - k - 1}\]

where n is the number of cases used to fit the model and \(k\) is the number of predictor variables in the model.

Because k is never negative, the adjusted \(R^2\) will be smaller - often times just a little smaller - than the unadjusted \(R^2\). The reasoning behind the adjusted \(R^2\) lies in the degrees of freedom associated with each variance.

In multiple regression, the degrees of freedom associated with the variance of the estimate of the residuals is n - k - 1, not n - 1. For instance, if we were to make predictions for new data using our current model, we would nd that the unadjusted R2 is an overly optimistic estimate of the reduction in variance in the response, and using the degrees of freedom in the adjusted R2 formula helps correct this bias.

Exercise \(\PageIndex{8}\)

There were n = 141 auctions in the mario_kart data set and k = 4 predictor variables in the model. Use n, k, and the variances from Exercise 8.10 to calculate \(R^2_{adj}\) for the Mario Kart model.9

Solution

\(R^2_{adj} = 1 - \frac {23.34}{83.06} \times \frac {141- 1}{141- 4 - 1} = 0.711\).

Exercise \(\PageIndex{9}\)

Suppose you added another predictor to the model, but the variance of the errors \(V ar(e_i)\) didn't go down. What would happen to the \(R^2\)? What would happen to the adjusted \(R^2\)?

Solution

The unadjusted \(R^2\) would stay the same and the adjusted \(R^2\) would go down.